Related Articles

“Like gold, U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation. Of course, the U.S. government is not going to print money and distribute it willynilly……..”

Ben S. Bernanke,

Federal Reserve Board Governor, November 21, 2002.

http://www.federalreserve.gov/boarddocs/speeches/2002/20021121/default.htm

When I originally read this two years ago, I had to read it through twice…I couldn’t believe it. Like many of you readers I saw all this coming. Look at my Straight Talk #3: Applying the Paddles to the US Economy from September 29, 2001 http://www.straighttalkonmining.com/docs/pdf/stom3.pdf. When the economy is in trouble, inflating the money supply is the path-of-least-resistance. You can toss money around and make everything seem okay – for the short term anyway. Now that George W. Bush has secured the presidency for the next four years, we all know that once his term ends, the problems both domestic and international he has faced will no longer be his responsibility and will be handed on to the next guy. Democracy is a great thing, but in the U.S. of A., pending elections can be enormously distracting, and more and more of a president’s term seems to be consumed by stumping for votes rather than governing.

When deflation threatens and you don’t respond by massive inflationary spending, the voters can and will hand you your head. President Grover Cleveland, faced with the fallout from the Bank Panic of 1893 stuck to his guns and refused the reinstatement of the mildly inflationary Sherman Silver Purchase Act. He believed in the sanctity of the Gold Standard, though he became enormously unpopular for it. The result of the 1894 mid-term election is unprecedented in history: the Democrats lost 113 seats in Congress. In the northeast, the Democratic congressional contingent was reduced from 88 to 9, and in 24 states the party no longer had congressional representation at all. (At the Democratic National Convention in 1896, Williams Jennings Bryan in an about-face would deliver his famous “Cross of Gold” speech…more about that in a future Straight Talk). In the Great Depression election of 1932, incumbent Herbert Hoover was soundly trounced by Franklin Roosevelt, winning the electoral votes of only 6 states.

When Bush took office he was given the near impossible task of forestalling the unraveling of the Greatest Equity Bubble of All Time. It was done by tax breaks and lowering the Fed Fund rate to almost zilch to spark a housing boom. Then, with the housing market running away, first as a safe-haven to the stock market, and soon thereafter as speculator heaven, those good little (but tapped-out) consumers took out home equity loans and splurged on SUV’s and continued the party. Meanwhile, Fed Chairman Alan Greenspan stuck his head in the sand and stated publicly that there was no housing bubble and that the surge was “due to immigrant purchases”. George was also fighting a war on two fronts: one domestic and two in Asia. I remember walking through Immigration at Miami International Airport and seeing new computer terminals stacked floor-to-ceiling that would collect information for the new Office of Homeland Security. Call me a cynic, but it’s easier to inject cash into the economy in the guise of war-spending than it is to push tax breaks through Congress.

Sure, you can’t print money and distribute it willy-nilly…

“By coordinating with fiscal policy, the Fed could even implement what is essentially the classic textbook policy of dropping freshly printed money from a helicopter. In this case, the Fed would monetize government debt that had been issued to finance a tax cut”.

Evan F. Koenig Vice-President, Jim Dolmas, Senior Economist, Research Department, Federal Reserve Bank of Dallas

May, 2003

http://www.dallasfed.org/research/indepth/2003/id0304.pdf

Take a look at the weblink. I love the graphic of the Chinook helicopter!

The twin elephants in the room that were not discussed in this election campaign are the trade imbalance and the budget deficit. Neither can be reduced to a sound-bite discussion or will fit in the 2 minute response time of the television debates. No candidate wanted to open that tin of worms, however, foreigners sure understand what’s going on:

Headlines, Friday, November 5, 2004:

Dollar Falls to Record Low Against Euro

NEW YORK (Reuters) – The euro hit a record high against the dollar above $1.2927 on Friday as the beleaguered U.S. currency weakened across the board in technically driven trading.

The dollar’s bounce from strong U.S. employment data earlier in the session proved fleeting, as dealers, concerned about record U.S. trade and budget deficits, saw an opportunity to sell it lower again.

This involved buying euros en masse, taking out options barriers around $1.2900, and then at the previous all-time high of $1.2927. The euro climbed above the high of $1.2927 hit on Feb. 18, touching a record peak around $1.2935, according to Reuters data.

Global policy-makers have recently appeared fairly tolerant of the dollar’s decline, and their laissez-faire attitude has encouraged investors to continue selling the U.S. currency. Some Federal Reserve officials recently signaled that the dollar would have to fall if the U.S. trade gap remains wide.

Aye, there’s the rub. The trade imbalance. Could it be possible that the U.S. is letting the dollar slide to make U.S. exports cheaper? Hmmmmm. It WAS discussed in that Dallas Fed paper above. Tricky business this. With the housing market topped out, and the lowest U.S. interest rates since 1958 failing to spark the Greatest Boom of All Time. What does one do next? Add in one more ingredient to the mix:

“Today, despite its recent surge, the average price of crude oil in real terms is still only three-fifths of the price peak of February 1981. Moreover, the impact of the current surge in oil prices, though noticeable, is likely to prove less consequential to economic growth and inflation than in the 1970s”.

Chairman Alan Greenspan, Federal Reserve Board

October 15, 2004.

http://www.federalreserve.gov/boarddocs/speeches/2004/200410152/default.htm

How many times have you heard this apology – “well it’s not really as bad as all that”. Isn’t it a little bit disingenuous to believe that higher oil prices are not going to translate into higher prices – for everything? With an economy already enormously strained by corporate and personal debt, spending deficits, and trade imbalances, and continuing to be pummeled by high fuel and commodity prices (steel, for instance), how many straws does it take to break this camel’s back? Is it any coincidence that gold is at a 16-year high against the dollar?

Being a Billionaire is not all it’s cracked up to be: Lessons from History

I love studying history. Not only do I find it enormously satisfying and entertaining, but it can also be enormously instructive, for, as Ambrose Bierce observed:

“There is nothing new under the Sun, but there are lots of old things we don’t know.”

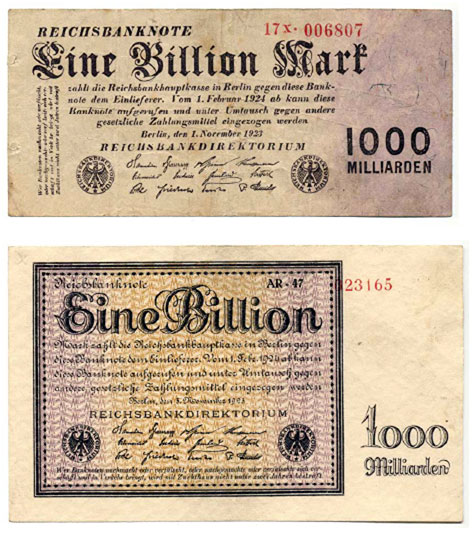

These two bank notes were issued during the infamous German Weimar Hyperinflation. The top is dated November 1, 1923. The bottom is dated November 5, 1923 (perhaps the plates were changed days later to a new design to instill confidence? It didn’t work!). The coin is a gold 20 German Mark piece from 1902, slightly smaller than a U.S. Quarter. In 1923, this gold coin was worth ten times the value of these two combined bank notes. That’s right. By the way, 1000 milliarden = 1,000,000,000,000, and so this little 20 Mark coin was equal to 20,000,000,000,000 of the paper Marks. The Mark was tod by the 20th November, when 12 zeros were arbitrarily lopped off the end and it became the Rentenmark. On the day that the Mark was extinguished the above notes together were equal to just US 46¢. If you want to show your children what inflation is all about, just print this out and show them the Exhibits A, B and C above. I know that over 95% of planet Earth it would take me about 5 minutes to convert that 100-year old coin into local currency for a steak dinner and a nice bottle of wine. The paper money is only valuable to a collector of arcana like myself.

These two bank notes were issued during the infamous German Weimar Hyperinflation. The top is dated November 1, 1923. The bottom is dated November 5, 1923 (perhaps the plates were changed days later to a new design to instill confidence? It didn’t work!). The coin is a gold 20 German Mark piece from 1902, slightly smaller than a U.S. Quarter. In 1923, this gold coin was worth ten times the value of these two combined bank notes. That’s right. By the way, 1000 milliarden = 1,000,000,000,000, and so this little 20 Mark coin was equal to 20,000,000,000,000 of the paper Marks. The Mark was tod by the 20th November, when 12 zeros were arbitrarily lopped off the end and it became the Rentenmark. On the day that the Mark was extinguished the above notes together were equal to just US 46¢. If you want to show your children what inflation is all about, just print this out and show them the Exhibits A, B and C above. I know that over 95% of planet Earth it would take me about 5 minutes to convert that 100-year old coin into local currency for a steak dinner and a nice bottle of wine. The paper money is only valuable to a collector of arcana like myself.

Here are some almost-not-to-be-believed extremes of the German Weimar Inflation:

“Petty crime, the crime of desperation, was flourishing. Pilfering had of course been rife since the war, but now it began to occur on a larger, commercial scale. Metal plaques on national monuments had to be removed for safe-keeping. The brass bell plates were stolen from the front doors of the British Embassy in Berlin, part of a systematic campaign unpreventable by the police even in the Wilhelmstrasse and Unter den Linden. Over most of Germany the lead was beginning to disappear from roofs. Petrol was siphoned from the tanks of motor cars. Barter was already a usual form of exchange; but now commodities such as brass and fuel were becoming the currency of ordinary purchase and payment. A cinema seat cost a lump of coal. With a bottle of paraffin one might buy a shirt; with the shirt, the potatoes needed by one’s family”.

When Money Dies: The Nightmare of the Weimar Collapse

Adam Fergusson

“In 1923, there were engaged on the production of notes for the Reichsbank…1,783 machines…(E)ven with assistance on so vast a scale the Bank was not in a position to supply the business world with a sufficiency of notes”.

German Monetary History in the First Half of the Twentieth Century

Robert L. Hetzel

You see, the money was depreciating so fast against common goods that entire print runs of notes were insufficient to satisfy demand for even a few hours.

——–

I have another little pamphlet that many readers may be familiar with: Fiat Money Inflation in France: How it Came, What it Brought, and How it Ended, by Andrew Dickson White. This discusses the currency experiment by the revolutionaries of the fledgling French Republic in 1790, which beggared the nation, fostered the Reign of Terror and ultimately brought Napoleon to power. The notes, known as Assignats were first printed in large denominations, but ultimately became the sole currency as all coinage was hoarded away. It took France 40 years to recover from the Assignat inflation. The numbers sound pretty small by today’s reckoning, but clearly horrified White, writing in 1912:

“Notwithstanding the fact that the paper currency issued was the direct obligation of the State, that much of it was interest bearing, and that all of it was secured upon the finest real estate of France, and that penalties in the way of fines, imprisonments, and death were enacted from time to time to maintain its circulation in value until it reached zero point and culminated in repudiation. The aggregate of the issues amounting to no less than the enormous and unthinkable sum of $9,500,000,000, and in the middle of 1797 when public repudiation took place, there was no less than $4,200,000,000 in face value of assignats and mandats outstanding; the loss, as always, falling upon the poor and the ignorant”.

The people responsible for putting France on the slippery slope of inflation – soon to mutate into hyperinflation – were clearly no dummies:

“It would be a mistake to suppose that the National Assembly, which discussed this matter [introduction of paper money], was composed of mere wild revolutionaries; no inference could be more wide of the fact. Whatever may have been the character of the men who legislated for France afterward, no thoughtful student of history can deny, despite all the arguments and sneers of reactionary statesmen and historians, that few more keen-sighted legislative bodies ever met than this first French Constitutional Assembly. In it were such men as Sieyès, Bailly, Necker, Mirabeau, Talleyrand, Dupont de Nemours and a multitude of others who, in various sciences and in the political world, had already shown and were destined afterwards to show themselves among the strongest and shrewdest men that Europe has yet seen”.

The inflating ended at 9 o’clock in the morning, 18th February, 1796, in the Place Vendome of Paris where the presses and paper to print Assignats were burned and the engraving plates smashed to bits with hammers in front of thousands of spectators.

When Bonaparte took the Consulship, at his first cabinet meeting he stated, “I will pay cash or pay nothing”. (“cash” meant gold)

It would be incredibly arrogant for any nation state to suppose itself permanently inoculated from hyperinflation. To do so would be hubris of the highest order – each time it has happened it began as a well-intentioned temporary inflating of the currency. Before saying that, “It couldn’t happen here”, here’s a partial list of countries that fell prey to hyperinflation in the last century: Hungary, Romania, Russia, Iraq, Italy, Yugoslavia, France, Germany, China, Vietnam, Mozambique, Ecuador, Peru, Croatia, Mexico, Venezuela, Turkey, Uruguay, Argentina, Brazil, Bolivia, Poland, Zaire, Austria, and Indonesia.

Understanding Drill Assays: Part 1

Pretty much every week I get shown some assays and asked on the spot if they are “any good”. Is there a quickie way of telling? Is there a “Drill Core Assays for Dummies” Handbook?

The short answer is “No”. It can be very hard to interpret drill hole results outside of any context – even for a career geologist.

So, how would an investor who is not a geologist or a geological engineer be able to tell if results are any good….is it a “buy” signal? A “sell”? A “hold”? Suppose it is the only information out there? Such things can be tough to decide, but I’ve boiled it down to a few guidelines.

Firstly, something that may sound rather obvious – if you aren’t already fully comfortable with the metric system, take time to learn it. If you don’t know what a metre is you’re setting yourself up for disaster. Any dictionary or encyclopedia should be able to give you conversion tables for weights and measures. The overwhelming majority of mining and exploration companies listed on the ASX, JSE, TSX, or AIM give assay values in grams per tonne and measure drill core lengths in metres.

Continuity and Geological Models

To make sense of press releases you have to navigate your way around the jargon we geologists use. Before any drilling takes place the geologist should always have an idea of which way the mineralization is trending. Geologists will often refer to the “strike” of the mineralized rock (you can think of it as “direction trend”), and the “dip” (which way the mineralization is tilted or inclined). As important as the metal content or “grade”; is demonstrating continuity – does the mineralization extend to depth and along the strike? You can’t “build tonnage” (incrementally increase the size of the mineralization through discovery) if you don’t have continuity. So the geologist will try to hit the buried mineralization with drill holes both along the trend, and at increasingly deeper levels. Sometimes geologists will use early information to drill “step out” holes, to test for continuity some distance away from earlier drill holes. They’re called step-out holes because they step away or jump some distance from the known to the unknown (sometimes these step-outs are a very real “leap of faith”!). A positive result from a step out hole will often make the share price rapidly move because it’s a way to quickly demonstrate size potential. If a step-out hole is successful, the geologist might want to track back in the opposite direction with “in-fill” holes. The geologist will also want to know how thick the mineralization is, and the best way to do that is to try to intersect it underground at right angles in drilling. A perfect right angle intersection will give you a “true thickness”. If you hit it at any other angle the mineralization will appear wider in the drill hole than it actually is in nature. This is a function of geometry. With a couple of drill holes at different inclinations you can use trigonometry and figure out the thickness (yes, High School Trig is important…tell your kids!) What any competent geologist will try to avoid is “drilling down the dip”. You can think of it this way: take any hardbound book and pretend that the closed book is an ore-bearing geological unit. Prop up one end so that the cover is inclined. Now take a pencil and rest the tip on the inclined cover. Orient the pencil so that it sticks straight up out of the cover at an angle of 90 degrees. That’s the best angle you should use if you were going to “drill” your book. A hole at this orientation is going to give you an accurate representation of the book thickness. However if you drilled through and down the spine of the book between the covers that’s like drilling down dip and will give you a false impression of thickness. Sometimes it can be tricky to figure the dip of mineralization, and it can often take a couple of cracks at it, drilling from different angles, to begin to sort it out. If a Company has been drilling narrow high grade veins and suddenly comes up with an extremely wide vein intersection, always be a bit skeptical and ask yourself if they may have drilled “down the dip”.

The geologist should also have a fair idea of a geological model. He may not have it completely understood at first pass but he or she should have it down to a few possibilities. This is one of the most important considerations in whether or not mineralization has the potential to eventually be “proved up” into an economic orebody. Let’s say that we’re drilling a gold-bearing quartz vein, which is “shallow” (near the surface). It might be possible to eventually mine that vein with a small open pit from surface. If it’s rich enough, it might pay you to afterwards go underground and sink a shaft to mine it from the subsurface. But if the vein is narrow and low grade, and only starts a couple of hundred metres down and not from surface, mining it will probably never be a paying proposition. Some quartz veins however can be very rich, and will support economic mining to very great depths. Let’s say you have a second orebody which is a vuggy silica unit (vuggy silica is very hard and porous quartz which has formed by replacing pre-existing rock, often by very acidic hotspring waters). The vuggy silica may be low grade, say 1 or 2 grams/tonne in gold and possibly 50 or even a hundred metres thick. Vuggy silica is usually a shallow mineralization type, and at those grades, if there is a considerable thickness, it can be very lucrative to mine it using open pit methods.

High grade has always moved markets, but today, in 2004, many mining people have noticed a trend in North America towards rewarding companies that come up with high grade numbers and paying less attention to anything else. My own personal “take” on this is that investors have been spoiled by the grades that have come out of Goldcorp’s Red Lake Mine. Many of the investors who were around in the early 1990’s during the last junior mining boom were permanently shaken out by the triple whammy of the Bre-X scandal, low gold prices, and expansion of the internet bubble which siphoned away venture capital (much of which historically went into junior mining). Over the last several years Bob McEwen has done a splendid job of promotion, giving the Red Lake Mine a high profile (even advertising on the radio!) so that many of the new crop of investors around today may falsely believe that all profitable gold mines have to have super high grade. The Red Lake mine has so much gold in some areas that visible gold can actually be mapped underground! You can draw a chalk line around the visible gold and enclose a sizable area. Proven and probable resources as of Dec 31, 2003 were 3.178 million tons at a grade of 1.23 oz/ton [42.17 g/t] gold for 4.939 million contained ounces. I was underground in 1987 when the mine was called the Dickinson, and was privileged to see such extreme high grade, which the miners explained to me they got into only twice or so a year. The miners call such places “jewel boxes”. I saw a drill bit clogged with gold, and two muckers horsing around trying to kick a piece of high grade down the drift (tunnel) with their steel-toed boots that was so heavy with gold it was reluctant to easily budge. Unless I get invited to go underground there again I don’t expect to see such high grade gold soon, if ever. I want to stress again, grades like these are pretty rare and the new discoveries over the next few years are not going to look like this.

You have to realize that the majority of highly profitable mining operations mine much lower average grades, and that many operating mines don’t have any “bonanza” grades like the example above. In fact, there are a number of senior mining companies that shy away altogether from high grade vein deposits. They may represent highly profitable low cost ounces but they typically represent a small number of contained ounces, say less than 1 million gold ounces – Red Lake is highly unusual. Many of the big Senior Gold Producers are trying to grow their reserves and want to do it in one foul swoop through finding a low grade but high tonnage and high number contained ounces deposit – like Barrick Gold has done with Pascua Lama (almost 300 million tons containing 16.862 million proven & probable gold ounces at a grade of 0.057 oz/ton [1.95 g/t], as of December 31, 2003). Exploration success doesn’t come easily and so most Senior Companies can only grow or even keep their reserve numbers level through mergers and acquisitions – witness the Harmony – Norilsk – Gold Fields – IAMGOLD bun fight currently in progress. High grade vein deposits are also very drill intensive (need to be very intensively [and expensively] drilled to accurately forecast the grade and tonnage), and the grade in veins can be erratic and veins themselves difficult to follow underground. Many Senior Miners want deposits that their engineers can plan for 5, 10 or even 20 years production, and they want to boast to fund managers that their reserve profile has been boosted by 3 or 5 million ounces. These big senior producers are looking to grow their ounces and are looking 5 or 10 years outboard. Meridian Gold took it on the chin recently from investors who didn’t like how much money was being spent on exploration, but if you’re going to find those low cost ounces, as Meridian has a track-record of doing – it gets pretty spendy.

Low grade big tonnage versus high grade low tonnage – both are important and both potentially highly valuable. As a rule-of-thumb many geos look at grammetres as to whether or not a drill result is interesting. Simply put, this is the grade multiplied by the width. A vein that is 5 metres wide and averages 60 g/t will represent 300 gram-metres, but so will a zone that is of lower grade, say 100 metres wide, grading 3 g/t. It of course would depend on the geological context as to which is the more interesting drill hole, but any exploration manager would be ecstatic to receive either result! An intersection of 10 gram-metres may or may not make it. An intersection of 50 gram-metres is pretty good; of 100 or 200 gram-metres is pretty gosh darn good, and anything higher becomes exceptional.

Minimum Mining Widths – Stretching the Interval

Fourteen years ago I received a spectacular assay of 800 g/t gold for a quartz vein I examined in Kirkland Lake, Ontario. The Vice-President of the company I worked for got busy the day the results were in, working out “if we average the grade out over 2 metres, we get x, and if we average over 3 metres we get y, and if we average it to 5 metres we get z”. Us guys in the field kind of rolled our eyes at this, because we knew that the vein was only 28 centimetres wide and that there was no gold in the wallrock (walls of the vein). He was “stretching the interval”. Now, there’s nothing wrong with someone “in house” making a few idle calculations. If you were to average the grade over 3 metres, assuming the wallrocks contained zero gold, you’d get 75 g/t gold over 3 metres, which is a pretty respectable number. However you’d be honour bound if not legally obligated to disclose in a press release that the gold occurs only over 0.28 metres width.

There’s a lot of gray area here, and there are a couple of things to consider. Firstly, a minimum mining width. This is the minimum width in which miners and machinery can safely work and is often legally mandated in a lot of jurisdictions by government Occupational Health and Safety folks, or by unions. Narrow mine workings can be difficult to get around which makes them unsafe in an emergency situation. In the old days, “rat holing” on the vein was a common practice. In a modern mining scenario it is not possible now, though it is common in places like South America, Mexico and China in artesanal mines. The thing to note here is dilution of grade from wall rock. In a modern mining scenario you have to take the minimum mining width – guts feathers and all, and can’t selectively mine narrow veins. Taking the barren wallrock is what is called “dilution”. In the above scenario it might be justifiable to stretch the interval to a minimum mining width of say 2 metres or so – but never to 5 metres.

The general industry practice is that assay intervals have to carry their own weight. This means that when you are calculating a weighted average amount of gold over a certain width you shouldn’t be including long sections of rock that is very low grade or barren in your calculation. It is however totally appropriate to include small sections in the width if the width represents one geological unit – say one big wide quartz vein with a couple of short sections here and there containing no or very low gold content. In a mining scenario you’d never leave these short sections behind as waste rock in any case, and you’d take the whole vein. This sounds a bit complicated and there is considerable latitude given to mining professionals when reporting grades and widths, but you should also be aware that this reporting can be open to abuse. When reporting drill intersections it’s good practice for a company to also report their highest individual assay alongside. Some companies even publish all the assays in table format – that way investors get the whole picture.

In Part 2, I’ll discuss the Nugget Effect, Cutting Assays and Stripping Ratios – more geo jargon you need to understand.